In the UK you only repay when your income is over £480 a week, £2,083 a month or £25,000 a year. If your income is below this, you simply do not repay, ever.

Does something like this not exist for american student loans? Am I right in assuming they just function like other loans?

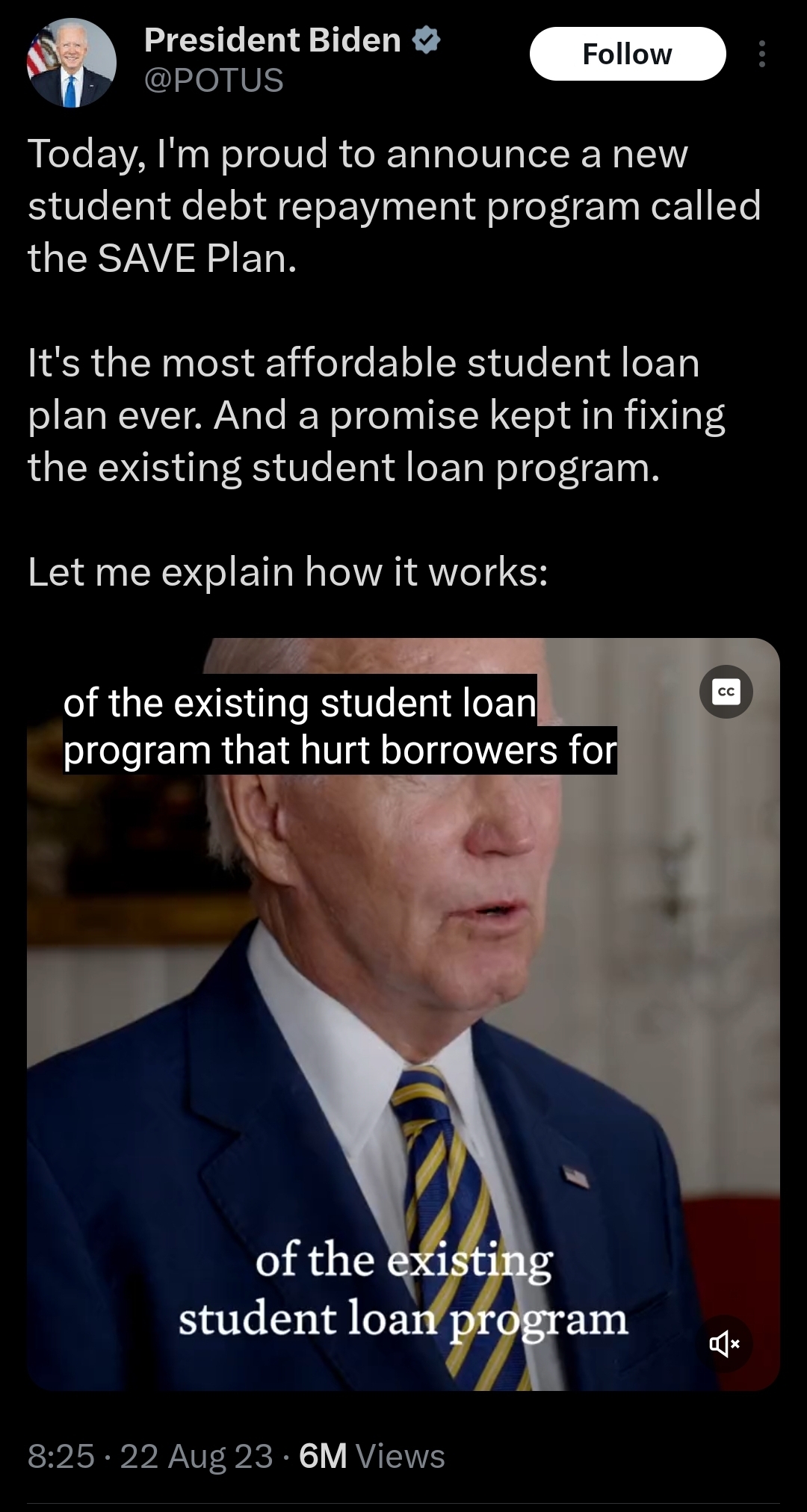

that's more or less what Biden is doing here. before, on income based repayment, one could have negative amortization, where a kid's principle would balloon/snowball if he couldn't cover the accruing interest. that's now been eliminated, and the effective income cap (for the income plan) has been/and will be substantially (imo) reduced.

An increase to 225pct of the federal poverty guideline, which I think should total out to something like $33000 for a single person w/ no dependents (or about the UK level, as I look up exchange rates). So you pay 5 or 10 pct (depending on undergrad or graduate loans) of the difference between your pre-tax income and 33000 (and thus, if you make 33000 or less, you pay nothing).

But, again, the big thing is that interest will not accrue, even if your monthly IDR payments are less than the debt servicing payment. That wasn't the case before. Back of the napkin math example, to illustrate: Say a kid had $240k in loans from four years to get a bachelors in the city (not unthinkable, if you're at a private school and paying w/loans for tuition and cost of living). Let's say unfortunately he can only get a barista job at $20/hr or AGI $40k out of school. With the improved IDR payment at 5pct of the difference of his income (40) and the guideline (33), his IDR required payments would be of $7000 * .05 = $350 yearly, or ~$30 / month. Pretty good. But (and my math might be off here, too conservative) the debt service payment on the total loan, at say 6pct, is going to be at least $15000 (or $1250/ month). So even if he only would need to pay ~$30 to avoid default, he still needs to pay an additional~$1200/ month (!) to avoid the principle of his loan increasing. Let's say annually, he's taxed for $6000, pays all his loan payments for $15000, pays $12000 for room/utilities, that leaves ~$600 a month for food, health insurance (though some may still be covered by parents insurance, I'm not quite sure on this) anything else you might want or need. This kid is getting royally fucked, he will not be paying down his loan at all, he will have no discretionary income. and while the new Biden regime is obviously not as good as it could be or should be, it eliminate this ghastly hypo.

{kind=link}

In the UK you only repay when your income is over £480 a week, £2,083 a month or £25,000 a year. If your income is below this, you simply do not repay, ever.

Does something like this not exist for american student loans? Am I right in assuming they just function like other loans?

that's more or less what Biden is doing here. before, on income based repayment, one could have negative amortization, where a kid's principle would balloon/snowball if he couldn't cover the accruing interest. that's now been eliminated, and the effective income cap (for the income plan) has been/and will be substantially (imo) reduced.

this is very good.

So what are the caps?

deleted by creator

that's the old rule. see my comment.

deleted by creator

An increase to 225pct of the federal poverty guideline, which I think should total out to something like $33000 for a single person w/ no dependents (or about the UK level, as I look up exchange rates). So you pay 5 or 10 pct (depending on undergrad or graduate loans) of the difference between your pre-tax income and 33000 (and thus, if you make 33000 or less, you pay nothing).

But, again, the big thing is that interest will not accrue, even if your monthly IDR payments are less than the debt servicing payment. That wasn't the case before. Back of the napkin math example, to illustrate: Say a kid had $240k in loans from four years to get a bachelors in the city (not unthinkable, if you're at a private school and paying w/loans for tuition and cost of living). Let's say unfortunately he can only get a barista job at $20/hr or AGI $40k out of school. With the improved IDR payment at 5pct of the difference of his income (40) and the guideline (33), his IDR required payments would be of $7000 * .05 = $350 yearly, or ~$30 / month. Pretty good. But (and my math might be off here, too conservative) the debt service payment on the total loan, at say 6pct, is going to be at least $15000 (or $1250/ month). So even if he only would need to pay ~$30 to avoid default, he still needs to pay an additional~$1200/ month (!) to avoid the principle of his loan increasing. Let's say annually, he's taxed for $6000, pays all his loan payments for $15000, pays $12000 for room/utilities, that leaves ~$600 a month for food, health insurance (though some may still be covered by parents insurance, I'm not quite sure on this) anything else you might want or need. This kid is getting royally fucked, he will not be paying down his loan at all, he will have no discretionary income. and while the new Biden regime is obviously not as good as it could be or should be, it eliminate this ghastly hypo.