I work a travel job where meals are covered, and on my first monthlong work order, napkin maths says I will have just under 10k at the end of it.

Coming from a life where I lived in overdraft and HEROES act was peak living, I have no real idea what to do with this much skrilla.

I use a budgeting app that autopulls from my acccounts, and those show that I spend about $1200 per month without rent expenses.

I aim to put about a third of this money inyo index funds, and do mutual aid where I can, but am wondering what are some things more experienced chapos can offer to take into consideration when budgeting.

Keep 3-6 months expenses in a High-Yield Savings Account and never touch it, ever. Eliminates nearly all financial stress and lets you actually breathe.

This. After that, get towards being debt-free.

The personal power you gain by not having a chunk of your mind locked into obligation cannot be underestimated.

Prioritize freedom and well-being, even when the cost is skimping. Then, once you're settled, use some of that extra skrill to buy from sources that are actually ethical, or that are making positive changes in the world.

It depends on how long you need this money to last. When is your next gig and will it pay out at the same rate? Are you in the US? Is this 1099 or W2 income?

It’d be good to sketch out what your short, medium and long term financial goals are. If you have an accurate picture of your recurring expenses then the rest of it can be used to allocate to your goals depending on priorities.

Really strict budgets are hard to obey and can cause more stress so having a general awareness of your financial condition, i.e. approximate balances of accounts and transaction activity, is often good enough but ymmv

About 75:25 W2 and untaxed per diem. In the lower 48 yuh.

I get little advance warning of what my work schedule ends up being.

The 1099 income requires you to pay employment taxes so make sure you track your expenses as they pertain to your work and you may need to make quarterly tax payments on that income. W2 income should have all of the withholdings so you should be ok with that.

After you cover your expenses then you can put amounts for savings and investments like a Roth IRA ($6,500 max per year) and the rest of it can be “living” money with which you can do whatever you wish. The more automatic the savings is the better to reduce the friction of additional tasks.

There is no “good” bank unfortunately and while credit unions are preferred they have geographic and/or membership constraints. If you don’t deal with cash then you can just use an online bank like Schwab where you can manage your checking and investment accounts.

Going back to your budget you should get an accurate picture of your recurring expenses including rent, food, utilities, insurance, phone, etc. then put several months (3-6 months is the standard) worth of those expenses aside in a savings account. I would add more for potential tax liabilities.

You said $1200 for expenses without rent. With rent if the average is $2400 total per month, then you should set aside 3-6 times that amount: $7200 - 14400. Seems crazy at first especially since it mostly just sits there but it means you can basically make any vehicle repair, cover most minor medical emergencies, pay deductibles, even supplement income if you become unemployed. Think of it as self-insurance where you pay the premiums to yourself. The balance can be built up over time.

After that you can see what is remaining and plan accordingly. You’ll have to revisit your plan periodically to make sure you’re reaching your savings and mutual aid goals.

Max out employer-matching 401k if you have it. Shove a lot of money in your IRA for tax purposes if it makes sense. Invest as much as you can as early as you can. Putting down 10% more in your 20's is going to be much more useful than putting 50% more in your 60's

High yield savings accounts are good but a lot of them require $100,000 to reach the top amount.

- Show

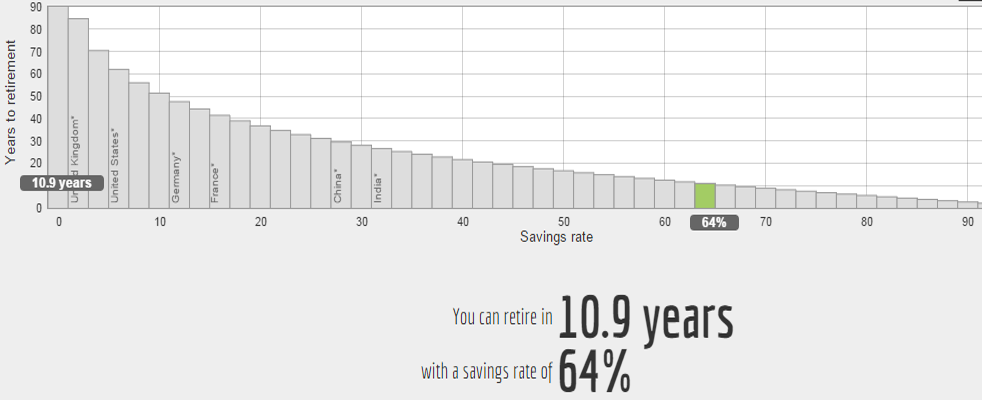

Just keep on like you were with a little bit more flexibility and woowoo finance bro says you can retire in 3 years.